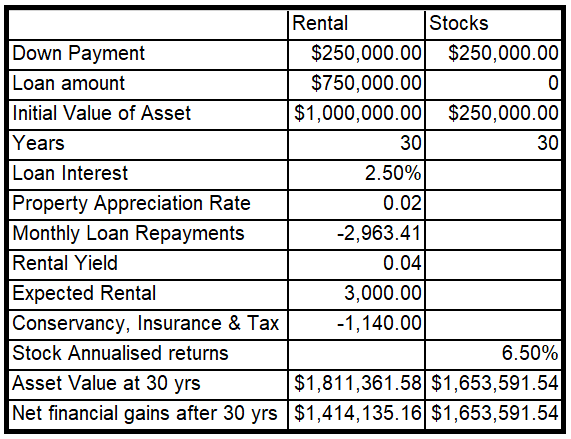

It is a dream of many Singaporean to save up enough money, buy a second property and become a landlord with a constant income stream. When I had the chance to do so, I decided to do some calculations to see if it is worth it, just to be sure before making a big decision like this. All I can say is that it is not as good as investing in the stock market based on current average returns (which are not too different from historical trends). Assuming the we have $250k to invest in the stock market or down pay a property, the below table shows the calculations for both scenarios.

From this calculation and making the assumptions stated in the table, it shows that the net financial gains of putting $250k in the stock market is better than using $250k for down payment to buy a $1M property. Additionally, I have not included other hidden costs that the landlord will have to bear: repair costs, agent fees, lost of rent when between tenancies, sprucing up the place to maintain rental yield, decreasing value after 30 years when holding a 99 year leasehold property, etc. They all add up to make being a landlord even less attractive.

That said, I am aware that this is a generalised statement: this is only one calculation and not representative of all investments in property or stocks. And depending on the rental/stock yield that you get, and changing market forces, the numbers may change in favor of one or the other. I certainly cannot claim to have a crystal ball into the future, no one can. Also, depending on your investment portfolio, being a landlord may be a good way of diversification. At the end of the day, what is most important is acknowledging that one investment plan is not better than the other, and more people should be open to investing in the stock market. If you really want to invest in property, I would suggest buying Real Estate Investment Trusts (REIT) where you get to own a share of commercial, industrial, retail or hospitality properties.

P.S. This is also based on my experience being both a landlord as well as a renter. For the past few years, my wife and I decided to rent out our condo, and rent a condo at a better location for us (nearer work). And I must say, that being a renter is better. When air-con spoil, just call landlord’s agent. No need to pay MCST, car park lot also free. The only down side is that it is not your property, i.e. cannot paint the walls if you feel like it… so you better look for a place that you really like.

Now that we decided to sell our place, it was clear to me that it will be better to use the proceeds of selling my place to invest in the stock market instead of planning to get a second property. This is based on my own experience as a landlord, as an investor in the stock market, and, of course, the above projection calculations (I did a few variants with different assumptions which gave me confidence in my decision). Another advantage of the stock market is that it is much more liquid compared to property. In other words, its much easier to buy and sell company stocks than property.

Hope this is useful information for you too. Anyway, there are more calculations that I did. Will share more when I have the time to write it down.